Friday, June 23, 2017

Tuesday, June 20, 2017

Do You Know How Much Equity You Have in Your Home?

CoreLogic’s latest Equity Report revealed that 91,000 properties regained equity in the first quarter of 2017. This is great news for the country, as 48.2 million of all mortgaged properties are now in a positive equity situation.

Price Appreciation = Good News for Homeowners

Frank Nothaft, CoreLogic’s Chief Economist, explains:

“One million borrowers achieved positive equity over the last year, which means risk continues to steadily decline as a result of increasing home prices.”

Frank Martell, President and CEO of CoreLogic, believes this is a great sign for the market in 2017 as well, as he had this to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion of home equity is one of the main drivers of improved mortgage performance. Since home equity is the largest source of homeowner wealth, the increase in home equity also supports consumer balance sheets, spending and the broader economy.”

This is great news for homeowners! But, do they realize that their equity position has changed?

According to the Fannie Mae’s Home Purchase Sentiment Index (HPSI), more homeowners are beginning to realize that they may have more equity than they first thought.

“This is only the second time in the survey’s history that the net share of those saying it’s a good time to sell surpassed the net share ofthose saying it’s a good time to buy.”

78.8% of homeowners have significant equity (more than 20%) in their homes today!

This means that many Americans with a mortgage have an opportunity to take advantage of today’s seller’s market. With a sizeable equity position, many homeowners could easily move into a housing situation that better meets their current needs (moving to a larger home or downsizing).

Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae spoke out on this issue:

“High home prices have led many consumers to give us the first clear indication we’ve seen in the National Housing Survey’s seven-year history that they think it’s now a seller’s market. However, we continue to see a lack of housing supply as many potential sellers are unwilling or unable to put their homes on the market…”

Bottom Line

If you are one of the many Americans who is unsure of how much equity you have built in your home, don’t let that be the reason you fail to move on to your dream home in 2017! Meet with a local real estate professional today, who can help you evaluate your situation and assist you along the way!

Source: Keeping Current Matters | The KCM Crew 062017

Monday, June 19, 2017

Buying Is Now 33.1% Cheaper Than Renting in the US

The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 3.5% less expensive in San Jose (CA), all the way up to 50.1% less expensive in Baton Rouge (LA), and 33.1% nationwide!

Other interesting findings in the report include:

- Interest rates have remained low and, even though home prices have appreciated around the country, they haven’t greatly outpaced rental appreciation.

- With rents & home values moving in tandem, shifts in the ‘rent vs. buy’ decision are largely driven by changes in mortgage interest rates.

- Nationally, rates would have to reach 9.1%, a 128% increase over today’s average of 4.0%, for renting to be cheaper than buying. Rates haven’t been that high since January of 1995, according to Freddie Mac.

Bottom Line

Buying a home makes sense socially and financially. If you are one of the many renters out there who would like to evaluate your ability to buy this year, meet with a local real estate professional who can help you find your dream home.

Source:Keeping Current Matters | KCM Crew 06192017

Wednesday, June 14, 2017

The TRUTH Behind the RENT vs. BUY Debate

In a blog post published last Friday, CNBC’s Diana Olnick reported on the latest results of the FAU Buy vs. Rent Index. The index examines the entire US housing market and then isolates 23 major markets for comparison. The researchers at FAU use a “‘horse race’ comparison between an individual that is buying a home and an individual that rents a similar-quality home and reinvests all monies otherwise invested in homeownership.”

Having read both the index and the blog post, we would like to clear up any confusion that may exist. There are three major points that we would like to counter:

1. The Title

The CNBC blog post was titled, “Don’t put your money in a house, says a new report.”The title of the press release about the report on FAU’s website was “FAU Buy vs. Rent Index Shows Rising Prices and Mortgage Rates Moving Housing Markets in the Direction of Renting.”

Now, we all know headlines can attract readers and the stronger the headline the more readership you can attract, but after dissecting the report, this headline may have gone too far. The FAU report notes that rising home prices and the threat of increasing mortgage rates could make the decision of whether to rent or to buy a harder one in three metros, but does not say not to buy a home.

2. Mortgage Interest Rates are Rising

According to Freddie Mac, mortgage interest rates reached their lowest mark of 2017 last week at 3.89%. Interest rates have hovered around 4% for the majority of 2017, giving many buyers relief from rising home prices and helping with affordability.

While experts predict that rates will increase by the end of 2017, the latest projections have softened, with Freddie Mac predicting that rates will rise to 4.3% in Q4.

3. “Renting may be a better option than buying, according to the report.”

Of the 23 metros that the study reports on, 11 of them are firmly in buy territory, including New York, Boston, Chicago, Cleveland, and more. This means that in nearly half of all the major cities in the US, it makes more financial sense to buy a home than to continue renting one.

In 9 of the remaining metros, the decision as to whether to rent or buy is closer to a toss-up right now. This means that all things being equal, the cost to rent or buy is nearly the same. That leaves the decision up to the individual or family as to whether they want to renew their lease or buy a home of their own.

The 3 remaining metros Dallas, Denver and Houston, have experienced high levels of price appreciation and have been reported to be in rent territory for well over a year now, so that’s not news…

Beer & Cookies

One of the three authors of the study, Dr. Ken Johnson has long reported on homeownership and the decision between renting and buying a home. The methodology behind the report goes on to explain that even in a market where a renter would be able to spend less on housing, they would have to be disciplined enough to reinvest their remaining income in stocks/bonds/other investments for renting a home to be a more attractive alternative to buying.

Johnson himself has said:

“However, in perhaps a more realistic setting where renters can spend on consumption (beer, cookies, education, healthcare, etc.), ownership is the clear winner in wealth accumulation. Said another way, homeownership is a self-imposed savings plan on the part of those that choose to own.”

Bottom Line

In the end, you and your family are the only ones who can decide if homeownership is the right path to go down. Real estate is local and every market is different. Meet with a local real estate professional who can explain what’s really going on in your area and can help you make the best, most informed decision for you and your family.

Source:Keeping Current Matters | KCM Crew 06142017

Thursday, June 8, 2017

69% of Buyers are Wrong About Down Payment Needs

According to a recent survey conducted by Genworth Financial Inc. at the Annual Mortgage Bankers’ Association Secondary Market Conference, mortgage professionals say that first-time buyers still believe a 20% down payment is necessary to buy in today’s market.

Nearly 40% of mortgage industry professionals surveyed believe that a lack of knowledge about the home-buying process is keeping potential buyers on the sidelines. Saving for a down payment is often cited as a huge barrier for first-time homebuyers to make the leap into homeownership.

If homeowners believe that they need a 20% down payment to enter the market, they also believe that they will have to wait years (in some markets) to come up with the necessary funds to buy their dream homes.

The greatest source of confusion cited in the survey results centered around down payments. The results are broken down in the chart below:

Rohit Gupta, CEO of Genworth Mortgage Insurance had this to say,

"While first-time homebuyers continue to drive the purchase market, we believe many are staying on the sidelines due to the misconception that a 20 percent down payment is required to secure a mortgage.There are various low down payment options available today that allow prospective homebuyers to reach their dreams of homeownership sooner. It is crucial that, as an industry, we proactively educate eligible borrowers about solutions that will enable them to buy a home when they're ready."

Bottom Line

Don’t let a lack of understanding of the home-buying process keep you and your family out of the housing market. Meet with a local real estate professional who can show you your options today!

Source:Keeping Current Matters | KCM Crew 06082017

Tuesday, June 6, 2017

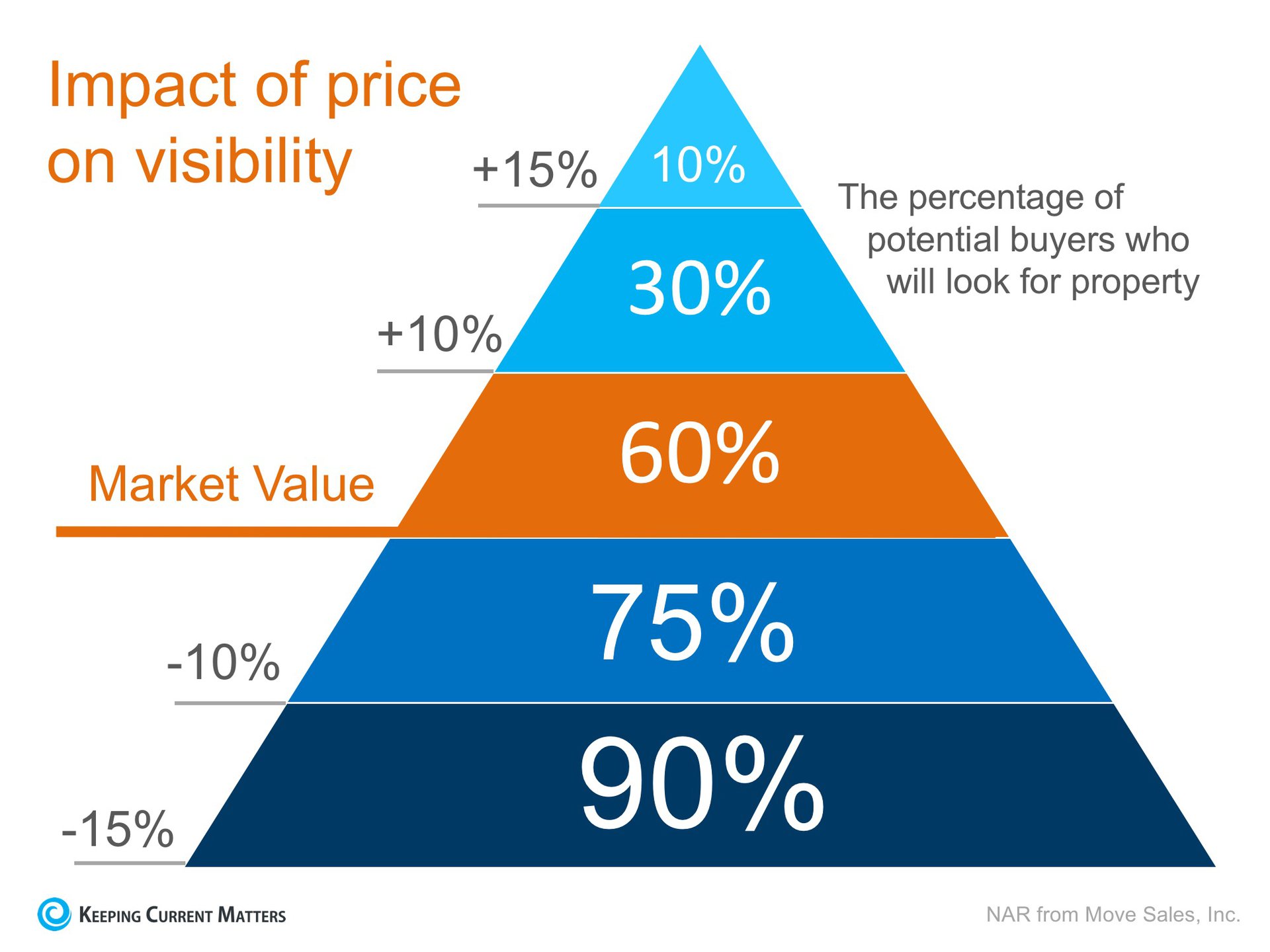

If Your Home Hasn’t Sold Yet… Definitely Check the Price!

The residential housing market has been hot. Home sales have bounced back solidly and are now at their fourth highest pace over the past year. Demand has remained strong throughout spring as many real estate professionals are reporting bidding wars with many homes selling above listing price. What about your house?

If your house hasn’t sold, it could be the price.

If your home is on the market and you are not receiving any offers, look at your price. Pricing your home just 10% above market value dramatically cuts the number of prospective buyers that will even see your house. See chart below.

Bottom Line

The housing market is hot. If you are not seeing the results you want, sit down with your agent and revisit the pricing conversation.

Source:Keeping Current Matters | KCM Crew 06062017

Monday, June 5, 2017

5 Reasons You Should Sell This Summer

Here are five reasons listing your home for sale this summer makes sense.

1. Demand Is Strong

The latest Buyer Traffic Report from the National Association of Realtors (NAR) shows that buyer demand remains very strong throughout the vast majority of the country. These buyers are ready, willing and able to purchase… and are in the market right now! More often than not, multiple buyers are competing with each other to buy a home.

Take advantage of the buyer activity currently in the market.

2. There Is Less Competition Now

Housing inventory is currently at a 4.2-month supply, well under the 6-months needed for a normal housing market. This means, in the majority of the country, there are not enough homes for sale to satisfy the number of buyers in that market. This is good news for home prices. However, additional inventory could be coming to the market soon.

There is a pent-up desire for many homeowners to move, as they were unable to sell over the last few years because of a negative equity situation. Homeowners are now seeing a return to positive equity as real estate values have increased over the last two years. Many of these homes will be coming to the market this summer.

Also, builder's confidence in the market has hit its highest mark in over 11 years. Experts are predicting that new construction of single-family homes will ramp up this summer.

The choices buyers have will continue to increase. Don’t wait until all this other inventory of homes comes to market before you sell.

3. The Process Will Be Quicker

Fannie Mae anticipates an acceleration in home sales that will surpass 2007's pace. As the market continues to strengthen, banks will be inundated with loan inquiries causing closing-time lines to lengthen. Selling now will make the process quicker & simpler. According to Ellie Mae’s latest Origination Insights Report, the time to close a loan has dropped to a new low of 42 days, after seeing a 12-month high of 48 days in January.

4. There Will Never Be a Better Time to Move Up

If you are moving up to a larger, more expensive home, consider doing it now. Prices are projected to appreciate by 4.9% over the next year, according to CoreLogic. If you are moving to a higher-priced home, it will wind up costing you more in raw dollars (both in down payment and mortgage payment) if you wait.

You can also lock in your 30-year housing expense with an interest rate around 4%right now. Rates are projected to increase in the next 12 months.

5. It’s Time to Move on with Your Life

Look at the reason you decided to sell in the first place and determine whether it is worth waiting. Is money more important than being with family? Is money more important than your health? Is money more important than having the freedom to go on with your life the way you think you should?

Only you know the answers to the questions above. You have the power to take control of the situation by putting your home on the market. Perhaps the time has come for you and your family to move on and start living the life you desire.

That is what is truly important.

Source:Keeping Current Matters | KCM Crew 06052017

Subscribe to:

Posts (Atom)