Source: Realty Times | Kenneth Johnson | 01082016

Friday, January 8, 2016

READY TO SELL YOUR FIRST HOUSE?

However long you have lived in your house, your choice to put it up for sale in the marketplace often comes with a ton of questions and of course, pressure. This is particularly true if it's your very first time through the sale process. Think about the next few points before getting going on the selling of your first house.

Determine to Sell

Before you'll be able to sell your house you should be completely prepared for all that it entails. Understand the marketplace as much as you can. You'll have to find qualified people who can help you list your home, and you need to be prepared to part with your house. Thinking of your property as only a house - without the sentimental connection - is going to generally allow you to to be realistic in regards to the value and total state of your property. With potential buyers utilizing the web increasingly to study future houses, you just get one opportunity to show them your house before they decide if they'd like to come see it and possibly buy it. Be up front about everything involved in your property, including cost.

Plan Ahead

A house can be sold quite fast, therefore it saves time and stress when you know where you are going to go once your house sells.

Find Trustworthy Realtors to Work With

The particular person or team you select will be someone(s) you are in direct contact with often. This means that ensuring that you find someone reputable and that you get along with is a vital element of selling your house. They are going to be your resource if you have questions in regards to the marketplace & prospective buyers. Plus they'll assist you with making a decision as to what price you need to list your house at in today's marketplace. It is necessary to seek out an agent that has a successful record of selling houses locally in your area that you can also trust.

Selling your first house becomes more and more easy when you're able to possess a strategy of where you are going to sell, a target of where you would like to be, and when you have someone working with you that you can trust. Make sure you're not unwilling to do what it will take to make your home as appealing and presentable as possible, and make sure you price it to sell.

Thursday, January 7, 2016

Obstacles to Homeownership: Perceived or Real?

Yesterday, we discussed the belief Americans have in homeownership and their desire to partake in this piece of the American Dream. We also discussed some of the obstacles preventing them from attaining that goal. However, studies have shown that that many of the obstacles mentioned are perceived, not real. A recent study by Fannie Mae, What Do Consumers Know About The Mortgage Qualification Criteria?, revealed that many consumers are either unsure or misinformed regarding the minimum requirements necessary to obtain a mortgage. Let’s break down three such challenges.

Down Payment

Perceptions

Many renters have mentioned that the lack of an adequate down payment is preventing them from moving forward with the purchase of a home. According to the Fannie Maereport:- 40% of all renters don’t know what down payment is required

- 15% think you need at least 20% down

- An additional 4% think you need at least 10% down

The Reality

There are programs offered by Fannie Mae, Freddie Mac and FHA that require as little as 3-3.5% down. VA and USDA loans offer 0% down programs. According to theNational Association of Realtors, the typical down payment for a first time buyer is 6%.Credit Score

Perceptions

Many renters have mentioned that the lack of an adequate credit score is preventing them from moving forward with the purchase of a home. According to the Fannie Maereport:- 54% of all renters don’t know what credit score is required

- 5% think you need at least a 740 credit score

The Reality

Many mortgages are granted to purchasers with a credit score of less than 700. According to Ellie Mae, the average credit score on a closed FHA purchase is 687 and the average credit score on all loans is 722.Back End Debt-to-Income Ratio (DTI)

Perceptions

Many renters have mentioned that they carry too much debt which is preventing them from moving forward with the purchase of a home. According to the Fannie Mae report:- 59% of all renters don’t know what DTI is acceptable

- 25% think you need at under 25%

- 7% think you need under 39%

The Reality

Lenders like to see a back-end ratio that does not exceed 36%. Fannie Mae’s maximum total DTI ratio is 36% of the borrower’s stable monthly income. The maximum can be exceeded up to 45% based on credit score and other requirements.Bottom Line

Don't let a lack of knowledge or misinformation keep your family from buying a home this year. Meet with a local real estate professional who can evaluate your ability to buy now!

Source: Keeping Current Matters / The KCM Crew / January 7, 2016

Tuesday, January 5, 2016

Top Reason to List Your House For Sale Now!

If you are debating listing your house for sale this year, here is the #1 reason not to wait!

Buyer Demand Continues to Outpace the Supply of Homes For Sale

The National Association of REALTORS’ (NAR) Chief Economist, Lawrence Yun recently commented on the inventory shortage:

“While feedback from REALTORS® continues to suggest healthy levels of buyer interest, available listings that are move-in ready and in affordable price ranges remain hard to come by for many would-be buyers.”

The latest Existing Home Sales Report shows that there is currently a 5.1-month supply of homes for sale. This remains lower than the 6-month supply necessary for a normal market and well below November 2014 numbers.

The chart below details the year-over-year inventory shortages experienced in 2015:

If you are debating listing your house for sale this year, here is the #1 reason not to wait!

Buyer Demand Continues to Outpace the Supply of Homes For Sale

The National Association of REALTORS’ (NAR) Chief Economist, Lawrence Yun recently commented on the inventory shortage:

“While feedback from REALTORS® continues to suggest healthy levels of buyer interest, available listings that are move-in ready and in affordable price ranges remain hard to come by for many would-be buyers.”

The latest Existing Home Sales Report shows that there is currently a 5.1-month supply of homes for sale. This remains lower than the 6-month supply necessary for a normal market and well below November 2014 numbers.

The chart below details the year-over-year inventory shortages experienced in 2015:

Housing Supply Year-Over-Year | Keeping Current Matters

Anything less than a six-month supply is considered a “Seller’s Market”. Bottom Line Meet with a local real estate professional who can show you the supply conditions in your neighborhood and assist you in gaining access to the buyers who are ready, willing and able to buy now!Source: Keeping Current Matters, KCM Crew, January 4, 2016

Thursday, December 24, 2015

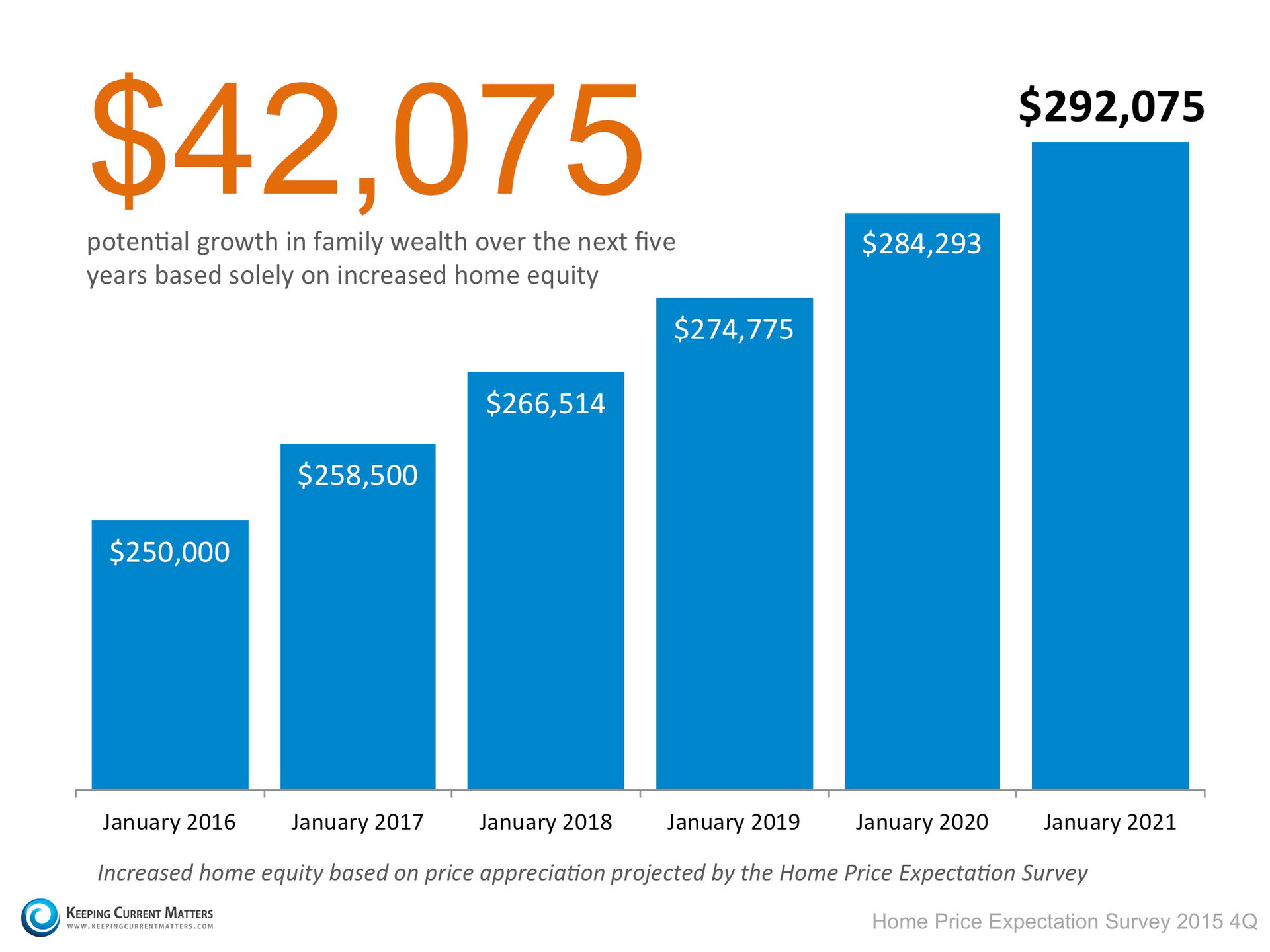

Building Family Wealth Over The Next 5 Years

As the economy continues to improve, more and more Americans are seeing their personal financial situations also improving. Instead of just getting by, many are now beginning to save and find other ways to build their net worth. One way to dramatically increase their family wealth is through the acquisition of real estate. For example, let’s assume a young couple purchases and closes on a $250,000 home in January. What will that home be worth five years down the road? Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists every quarter. They ask them to project how residential prices will appreciate over the next five years. According to their latest survey, here is how much value that $250,000 house will gain in the coming years.

Over a five year period, that homeowner can build their home equity to over $40,000. And, in many cases, home equity is large portion of a family’s overall net worth.

Bottom Line

If you are looking to better your family’s long-term financial situation, buying your dream home might be a great option.Source: Keeping Current Matters / The KCM Crew / December 2015

Thursday, December 17, 2015

FSBO, List Again or OTM? A Seller’s Dilemma

At the end of December, in every region of the country, hundreds of homeowners have a tough decision to make. The ‘listing for sale agreement’ on their house is about to expire and they now must decide to either take their house off the market (OTM), For Sale by Owner (FSBO) or list it again with the same agent or a different agent. Let’s assume you or someone you know is in this situation and take a closer look at each possibility:

Taking Your Home off the Market

In all probability, after putting your house on the market and seeing it not sell, you’re going to be upset. You may be thinking that no one in the marketplace thought the house was worthy of the sales price. Because you are upset, you may start to rationalize that selling wasn’t that important after all and say,“Well, we didn’t really want to sell the house anyway. This idea of making a move right now probably doesn’t make sense.”Don’t rationalize your dreams away. Instead, consider the reasons you decided to sell in the first place. Ask your family this simple question:

“What made us originally put our home up for sale?”If that reason made sense a few months ago when you originally listed the house, chances are it still makes sense now. Don’t give up on what your family hoped to accomplish or on goals your family hoped to attain. Just because the house didn’t sell during the last listing contract doesn’t mean the house will never sell or that it shouldn’t be sold.

Re-Listing with your Existing Agent

For whatever reason, your house did not sell. Perhaps you now realize how difficult selling a house may be or that the listing price was too high, or perhaps you’re now acknowledging that you didn’t exactly listen to your agent’s advice. If that is the case, you may want to give your existing agent a second chance. That’s a perfectly okay thing to do. However, if your agent didn’t perform to the standard they promised when they listed your home you may want to either FSBO or try a different agent.For Sale by Owner

You may now believe that listing your house with an agent is useless because your original agent didn’t accomplish the goal of selling the house. Trying to sell the house on your own this time may be alluring. You may think you will be in control and save on the commission. But, is that true? Will you be able to negotiate each of the elements that make up a real estate transaction? Are you capable of putting together a comprehensive marketing plan? Do people who FSBO actually ‘net’ more money? If you are thinking about FSBOing, take the time to first read: 5 Reasons You Shouldn’t For Sale by Owner.List with a New Agent

After failing to sell your home, you may no longer trust your agent or what they say. However, don’t paint all real estate professionals with that same brush. Have you ever gotten a bad haircut before? Of course! Did you stop getting your hair cut or did you simply change hair stylists? There is good and bad in every profession—good and bad hair stylists, agents, teachers, lawyers, doctors, police officers, etc. And just because there are good and bad in every line of work doesn’t mean you don’t call on others for the products and services you need. You still get your haircut, see a doctor, talk to a lawyer, send your kids to school, etc.Bottom Line

You initially believed that using an agent made sense. It probably still does. Contact a local real estate professional and discuss the possibilities.Source: Keeping Current Matters / The KCM Crew / 12172015

Tuesday, December 15, 2015

Selling Your House? 5 Reasons You Shouldn’t For Sale By Owner

In today's market, with homes selling quickly and prices rising, some homeowners might consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons this might not be a good idea for the vast majority of sellers. Here are five of those reasons:

1. There Are Too Many People to Negotiate With

Here is a list of some of the people with whom you must be prepared to negotiate if you decide to For Sale By Owner:- The buyer who wants the best deal possible

- The buyer’s agent who solely represents the best interest of the buyer

- The buyer’s attorney (in some parts of the country)

- The home inspection companies, which work for the buyer and will almost always, find some problems with the house

- The appraiser if there is a question of value

2. Exposure to Prospective Purchasers

Recent studies have shown that 89% of buyers search online for a home. That is in comparison to only 20% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home. Do you?3. Results Come from the Internet

Where do buyers find the home they actually purchased?- 44% on the internet

- 33% from a Real Estate Agent

- 9% from a yard sign

- 1% from newspaper

4. FSBOing has Become More and More Difficult

The paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 8% over the last 20+ years. The 8% share represents the lowest recorded figure since NAR began collecting data in 1981.5. You Net More Money when Using an Agent

Many homeowners believe that they will save the real estate commission by selling on their own. Realize that the main reason buyers look at FSBOs is because they also believe they can save the real estate agent’s commission. The seller and buyer can’t both save the commission. Studies have shown that the typical house sold by the homeowner sells for $210,000 while the typical house sold by an agent sells for $249,000. This doesn’t mean that an agent can get $39,000 more for your home as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense.Bottom Line

Before you decide to take on the challenges of selling your house on your own, sit with a real estate professional in your marketplace and see what they have to offer.Source: Keeping Current Matters, The KCM Crew 12152015

Thursday, December 10, 2015

You Will Need to Sell Your Home Twice

A recent post on “The Home Story”, a site published by Fannie Mae, explained the difference between the price a seller may get for their home and the value an appraiser might assign the property.

The Sales Price

Of course, most sellers want to maximize the value they get for the house. However, the price they set might not be reflective of the other comparable homes in the neighborhood. As the article stated:“People tend to view their homes emotionally, and that can become quickly apparent when they decide to sell.”That doesn’t mean that the home won’t necessarily sell for that price. A seller can set an asking price and actually have a buyer agree to that price. However, that value may not be necessarily in agreement with what most buyers are willing to pay. For example, one person can view a property, determine it is exactly what they are looking for and well worth the asking price, whereas another person could look at the same property and feel the asking price is too high. Steven Corbin, Director of Valuation in Fannie Mae’s CPM Real Estate division gives an example:

“Someone may have driven by the property countless times, and they really want to live in that house. So in reality they may overbid for that property. This would be a situation where the actions of a specific buyer do not represent the actions of a typical buyer.”

The Appraised Value (or Market Value)

Fannie Mae explains what they look for when appraising the house:“When a contract is established on a property, an appraised value is determined by a professional real estate appraiser. The appraiser works on the lender’s behalf to determine that value by taking many factors into consideration, including the neighborhood, the value of properties of similar size and construction, and even such things as the type of fixtures on the premises and layout of the floor plan.”Corbin adds:

“From a lending perspective, a bank would want to know the probable price a typical buyer would offer for the property. That’s what an appraiser would set as the market value.”

The Challenge when Sales Price and Appraisal Value are Different

If the appraiser comes in with a value that is below the agreed upon sales price, the lending institution might not authorize the mortgage for the full amount a buyer would need to complete the transaction. Quicken Loans actually releases a Home Price Perception Index (HPPI) that quantifies the difference between what sellers and appraisers believe regarding value. The HPPIrepresents the difference between appraisers’ and homeowners’ opinions of home values. Currently, there is approximately a 2% difference between what homeowners believe their home to be worth and what appraisers value that same home. On a $300,000 sale that would be a $6,000 difference. That could be a challenge that might prevent the home sale proceeding to the closing table. Quicken Loans Chief Economist Bob Walters recently commented on this issue:“The more homeowners are in line with appraisers, the easier it will be to refinance their mortgage and easier for those looking to buy a home. If the two are aligned, it eliminates one of the top stumbling blocks in the mortgage process.”

Bottom Line

Every house on the market has to be sold twice; once to a prospective buyer and then to the bank (through the bank’s appraisal). In a housing market where supply is very low and demand is very high, home values increase rapidly. One major challenge in such a market is the bank appraisal. If prices are jumping, it is difficult for appraisers to find adequate comparable sales (similar houses in the neighborhood that closed recently) to defend the price when performing the appraisal for the bank. With escalating prices, the second sale might be even more difficult than the first. That is why we suggest that you use an experienced real estate professional to help set your listing price.

Source: Keeping Current Matters/The KCM Crew/12102015

Subscribe to:

Posts (Atom)